The U.S. Department of Commerce has recently made adjustments to the preliminary tariffs imposed on crystalline silicon photovoltaic cells and modules from Cambodia, Malaysia, Thailand, and Vietnam, following an investigation. The final ruling is expected to be released on April 18, 2025.

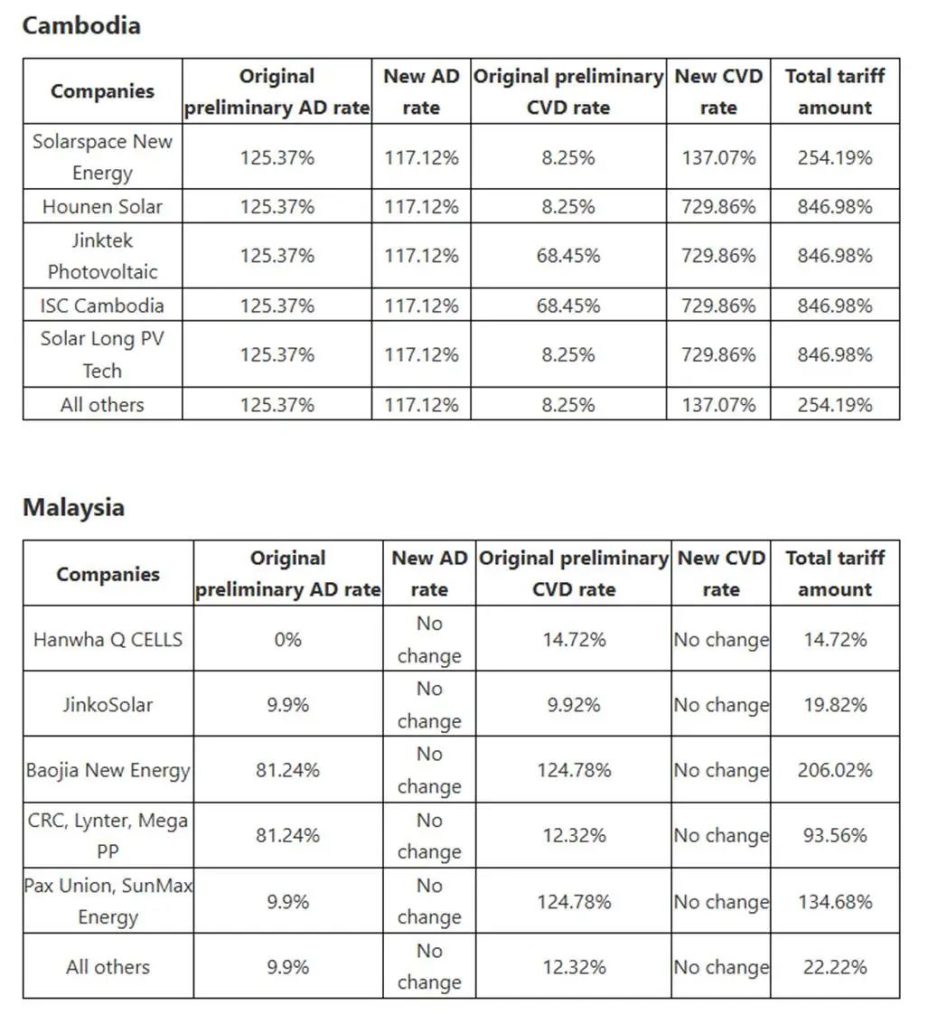

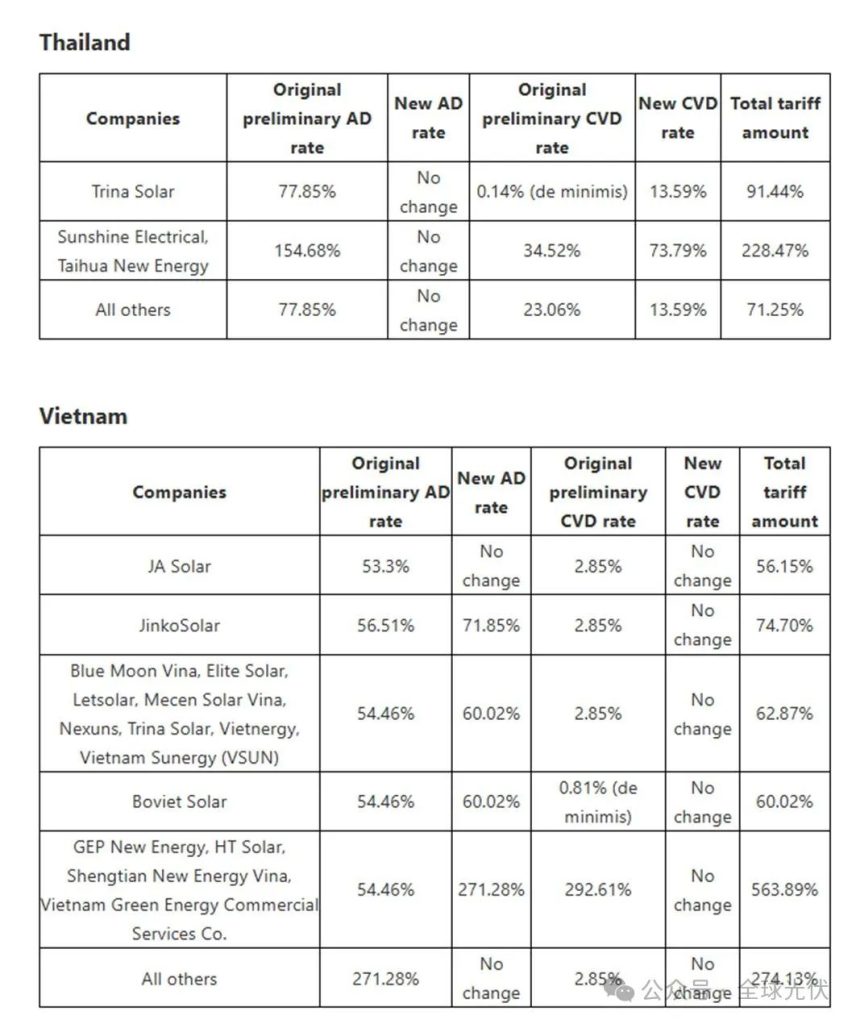

The tariffs before and after adjustment for various companies in these four countries, in response to anti-dumping and countervailing duty cases, are as follows:

The proposal for this tariff adjustment originated from a petition by seven U.S. solar manufacturers, including First Solar and Swift Solar. These companies alleged that the low-priced dumping of photovoltaic products from Southeast Asia had severely disrupted the U.S. domestic market and threatened the development of the U.S. photovoltaic industry.

As seen in the chart, specific tariffs have been imposed on Chinese companies such as JinkoSolar, Trina Solar, JA Solar, and Boviet Solar. Except for Hanwha, which has an anti-dumping tariff rate of 0% in Malaysia, all companies with factories in Southeast Asia are subject to varying degrees of tariffs when exporting to the United States. The adjustments are significant, with total tariffs ranging from a minimum of 14.72% to a maximum of 846.98%.

Since initiating the “anti-dumping and anti-subsidy” investigation against Chinese photovoltaics in 2012, the United States has imposed five rounds of trade sanctions. However, Chinese companies have continuously circumvented these restrictions through capacity transfers to Southeast Asia. In 2024, the four Southeast Asian countries accounted for more than 80% of U.S. imports of photovoltaic modules, with about 70% of this capacity dominated by Chinese companies. The U.S. Department of Commerce is now attempting to cut off China’s photovoltaic export path through Southeast Asia by imposing ultra-high tariffs on the grounds of “circumventing anti-dumping measures.”

Taking Vietnam as an example, with the increase in comprehensive tariffs, the cost of exporting modules to the United States will rise to 0.50-0.60 per watt, far higher than the 0.30-0.35 per watt for U.S. domestic modules, completely eroding their competitiveness. Additionally, the European Union’s Carbon Border Adjustment Mechanism (CBAM) requires the disclosure of component carbon footprints, while the U.S. Inflation Reduction Act (IRA) mandates a localization rate exceeding 50%. Under this double pressure, Chinese companies need to introduce green energy and localized raw materials into their Southeast Asian factories, further increasing costs.

According to 2024 data, Southeast Asian photovoltaic module capacity has shrunk to 78.8GW. Overall, the proportion of Chinese photovoltaic companies’ capacity in Southeast Asia is not high. However, in the long run, being forced out of the U.S. market is not impossible.

The four Southeast Asian countries have 59.8GW of battery capacity and 90.6GW of module capacity. Under high tariffs, these capacities may shift to Europe, the Middle East, or return to China. Companies such as JinkoSolar, JA Solar, and Longi have planned to supply modules through factories in the United States, while Trina Solar is circumventing IRA subsidy restrictions through equity swaps.

As of 2024, U.S. module capacity stands at only 13GW and relies on imports of silicon wafers and batteries from Chinese companies. With the suspension of subsidies under the IRA, more uncertainty has been added to the supply of domestic capacity in the United States.

{kind=link}