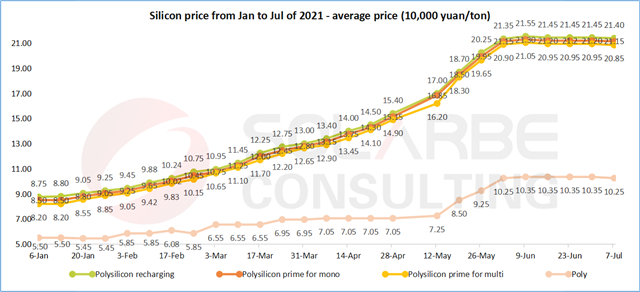

Silicon: price reduction raises industry expectation

In the first week of July, the price of silicon finally ushered in a high point of decline, clear despite slow. It will take several years to reach carbon emission peak, but the silicon price has reached its peak. According to the statistics of the silicon material production expansion and the analysis of the installation expectation, Solarbe Consulting believes that the price will not reach a higher level.

In the past two months, downstream enterprises have been reducing the demand by reducing the operating rate, putting pressure on the price of silicon materials. After the first price reduction of wafers and cells last week, the price of silicon has finally started to decrease, which has brought confidence to the photovoltaic industry.

According to the calculation of the Chinese Silicon Industry, the transaction price of the mainstream market remained stable this week, and that of enterprises with new orders remained unchanged on a month on month basis, but no transaction during the high price range this week led to a decline of the average price calculation result. Solarbe Consulting believes the trend will continue, forcing the silicon price down. Whether the supply of materials for the new production capacity of silicon wafer has been determined will be an important factor affecting the falling range of silicon material price.

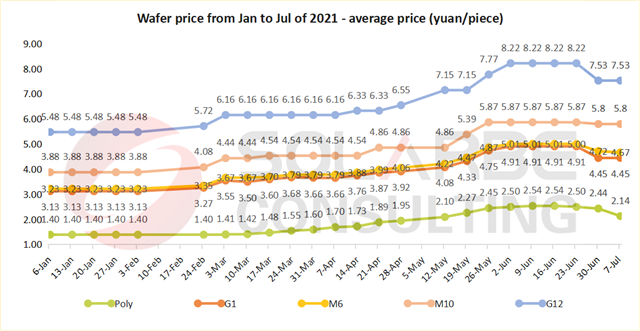

Wafer: mono remains stable while poly shows a decline

It is difficult to determine the reaction time of each link in the industrial chain to the product price changes of related links, but the reaction of the adjacent two links is the fastest, and it takes a certain time to transmit to the downstream links. Because the price of wafers was adjusted first last week, in the purchase negotiation of new silicon material orders, for the sake of cost and profit, the high price range was not accepted, resulting in the decrease of average transaction price of silicon material and favorable market trend. At the same time, the price reduction of raw materials also brings hope to silicon wafer enterprises and downstream cell and module enterprises.

This week, the price of monocrystalline wafer was the same as last week, the average price of polycrystalline was RMB 2.14 yuan/piece, a month on month decrease of 12.32%, with significantly reduced demand and market share.

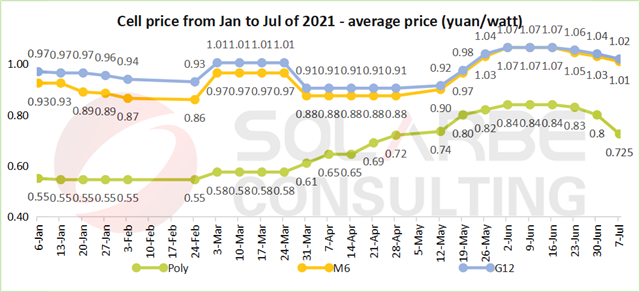

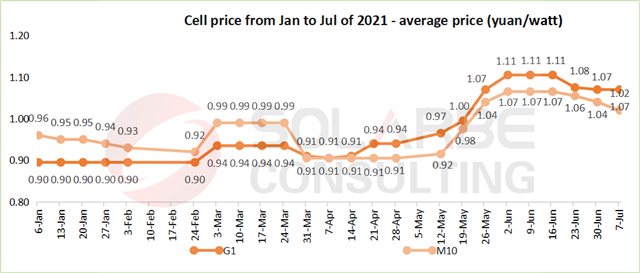

Cell: continue to reduce, seize the market

This week, the price of cells continued to decline except G1. The mono cells of M6, M10 and G12 decreased by RMB 0.02 yuan/watt, a month-on-month decrease of 1.94%, 1.92% and 1.92% respectively. Due to the limited output of G1 cells, the supply and demand are relatively stable compared with other sizes of cells, and the price is kept at RMB 1.07 yuan/watt.

The market price of cells is dominated by Tongwei and Aikosolar. Under the premise of stable price of wafers, the price of cells will continue to be reduced, which requires high cost management. If the price is low enough, vertical integration enterprises would be willing to purchase.

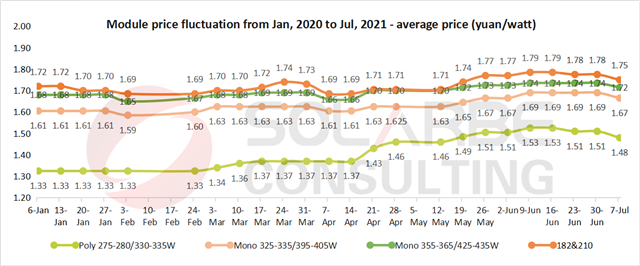

Modules: price reduction, profit transmission

This week, the prices of all modules were reduced by RMB 0.02 – 0.03 yuan/watt. Due to the price reduction of cells, the pressure of module enterprises is relieved, and more profits can be transferred to terminal investment enterprises to further stimulate the installation. In comparison, there are two main reasons why the price of module is lower than that of cell terminals. One is to make up for the previous losses. The other is that the price of packaging materials is still fluctuating, and the non silicon cost is unstable.

{kind=link}