China’s polysilicon industry is basically developed under the promotion of the development of China’s photovoltaic industry since 2005. All the way through overcapacity, elimination and merger, the industry concentration has been increasing. In the photovoltaic industry chain, silicon material requires high technical threshold, large investment and the longest production expansion cycle, which contains certain industry monopoly. Therefore, polysilicon manufacturing covers a relatively small part of the whole photovoltaic industry chain.

Polysilicon is the most important and basic functional material in semiconductor industry, electronic information industry and solar cell industry. Nowadays, polysilicon is the main photovoltaic material, with a market share over 90%, and it is still the mainstream material of solar cells in a long run.

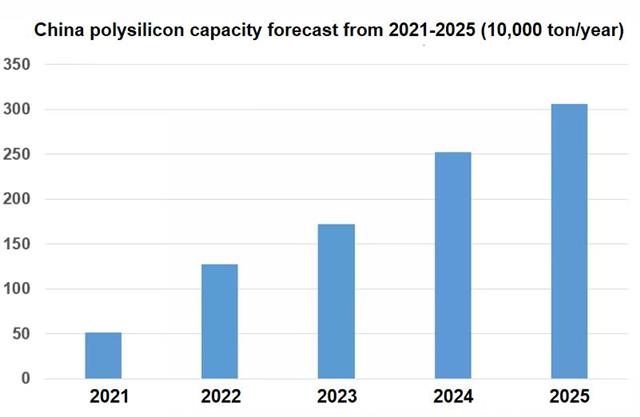

By the end of 2020, China’s polysilicon capacity reached 420,000 tons. The output reached 396,000 tons, a sharp increase of 15.1% year-on-year, accounting for 75.3% of the total global output. The production capacity and output will continue to increase substantially in the next five years. According to the statistics of consulting organization AsiaChem, there are a total of 17 polysilicon projects under construction or planned in China in 2021. If all projects are put into operation, it is expected that the capacity will exceed 3 million tons by 2025, by which can produce 1,000 GW of wafers. Then polysilicon overcapacity is inevitable.

The price of domestic polysilicon market has risen rapidly since the fourth quarter of 2020, which has risen from RMB 60 yuan/kg to 200 yuan/kg within few months. The soaring price leads to the shortage of wafer, the constant change of the price of cell and module, and even the price of backsheet, tracker and inverter.

Since the second half of 2020, traditional enterprises have successively announced the expansion of production, together with participation of new players such as Xinjiang Jinnuo, Jiangsu Runyang, Baofeng Energy and other enterprises, which invested in the construction of production capacity to enter the silicon material arena.

With the recovery of photovoltaic downstream demand and the substantial expansion of silicon wafer enterprises, the relationship between supply and demand of polysilicon is gradually reversed. Although the domestic demand for polysilicon will continue to grow, with the completion and commissioning of a large number of new polysilicon projects, the trend of excess capacity of polysilicon will be strengthened in the future.

{kind=link}