According to the Central Electricity Authority of India, the cumulative installed PV capacity in India reached 97.9GW in 2024, with new installations of approximately 24.5GW, more than doubling compared to 2023. With the advancement of government tenders and incentive measures, the Indian PV market is expected to continue growing, contributing to the global energy transition. Below is an introduction to India’s major PV policies and demand forecasts for 2025.

Project-Specific Incentive Policies Driving Indian PV Demand

- Centralized & Industrial and Commercial Projects

Centralized Project Policy: In 2014, the Indian government launched the Development of Solar Parks and Ultra Mega Solar Power Projects, aiming to add 40GW of PV capacity by the 2026 fiscal year (March 31, 2026). Each megawatt (MW) is eligible for a subsidy of 2 million Indian rupees (approximately 24,000)or301.03 billion) allocated for subsidies to build ground-mounted power stations. Notably, CPSU subsidies can be used in conjunction with those from the aforementioned solar park and ultra-mega solar power project development plans.

Industrial and Commercial Projects: The most notable policy is the Green Energy Open Access Rules (GEOA) introduced in 2022, which allows renewable energy buyers to directly sign power purchase agreements (PPAs) with sellers and only pay grid usage fees and other charges. The minimum power purchase requirement for buyers has also been reduced from the initial 1MW to the current 100kW, boosting demand for smaller-scale industrial and commercial PV projects.

- Residential & Off-Grid Projects

Residential Projects: In February 2024, India launched the PM-Surya Ghar scheme, targeting 40GW of new distributed PV installations by the 2026 fiscal year. The scheme will invest 750 billion Indian rupees and provide up to 300kWh of free electricity per month for ten million households. Subsidy amounts vary based on project size: for projects less than 2kW, each kilowatt (kW) receives a subsidy of 30,000 Indian rupees (approximately 360);forthe2−3kWrange,thefirst2kWreceivethesamesubsidy,andtheremainingkWreceives18,000Indianrupees(approximately216) per kW; for projects larger than 3kW, a fixed subsidy of 78,000 Indian rupees (approximately $936) is provided.

Off-Grid Projects: The primary program is the PM-KUSUM scheme launched in 2019, with a total budget of 344.2 billion Indian rupees (approximately $4.13 billion), targeting 34.8GW of new PV installations. This includes the construction of 500kW-2MW PV power stations, the installation of 1.4 million off-grid PV agricultural pumps, and the conversion of 3.5 million grid-connected agricultural pumps to PV power generation. Depending on the region and project type, subsidies of over 30% of the total project cost are provided by the central and state governments.

Stimulating Demand-Side Policies Alongside Localization Manufacturing

To keep pace with the growing demand for PV products, India is actively promoting localization manufacturing policies. In 2022, India imposed a Basic Custom Duty (BCD) on imported PV products, with tax rates of 25% for batteries and 40% for modules. Additionally, in 2021, India approved the Production Linked Incentive Scheme (PLI), investing a total of 240 billion Indian rupees (approximately $2.88 billion) in two phases to subsidize the construction of PV capacity from upstream polysilicon to downstream modules. Subsidy amounts are calculated based on sales, localization levels, and product conversion efficiency. The tendered capacity under this scheme is expected to be operational by 2026. Lastly, there is the Approved List of Models and Manufacturers (ALMM), which stipulates that government-related projects must use locally manufactured modules from the list. As of January 2025, the listed module capacity reached 64.6GW, sufficient to meet India’s terminal demand. Furthermore, from June 2026, India will introduce an ALMM battery list, further requiring government projects to use locally assembled modules with locally produced batteries.

India’s PV Market Outlook for 2025

Overall, due to India’s relative lack of battery capacity due to insufficient technological reserves, even with a 25% BCD on imported batteries, Chinese imported batteries still have a competitive advantage. After the implementation of the ALMM module list, the Indian market is dominated by locally assembled modules using Chinese batteries. If the ALMM battery list is implemented as scheduled in 2026, the timely commissioning of Indian battery capacity will be crucial. On the other hand, due to the cost-effectiveness of Chinese batteries, if government project components must then use locally assembled batteries, the increase in project costs may adversely affect the future development of the PV market.

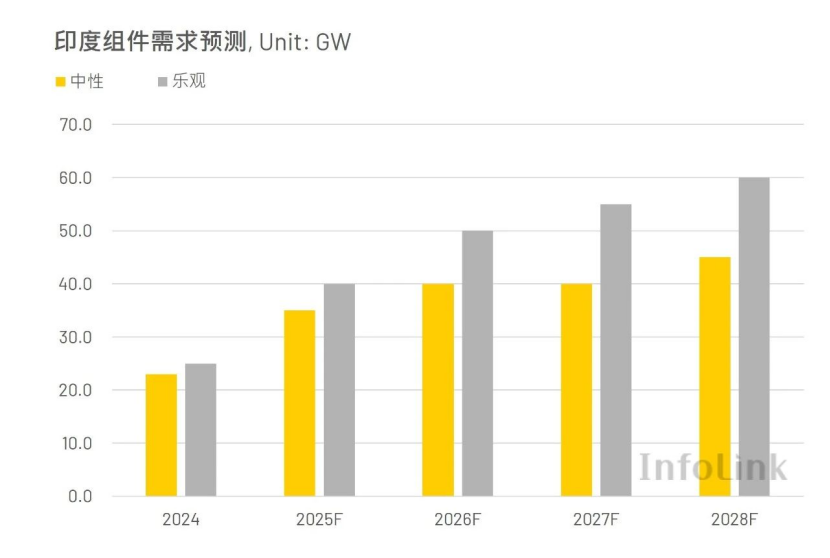

From the demand-side policy perspective, since the Development of Solar Parks and Ultra Mega Solar Power Projects, PM-Surya Ghar, and PM-KUSUM all have installation targets set for the 2026 fiscal year, and under the policy framework of the National Electricity Plan (NEP), India must reach a cumulative installed PV capacity of 280GW by 2030, representing an average annual addition of 30GW. Therefore, with the continuation of various subsidies and policies, 2025 will be a crucial period of development for the Indian PV market. InfoLink expects PV demand to reach 35-40GW in 2025.

{kind=link}