In the first half of 2024, China’s solar industry has shown resilience amid challenging market conditions, with over 800 billion RMB in new contracts and a flurry of project activities.

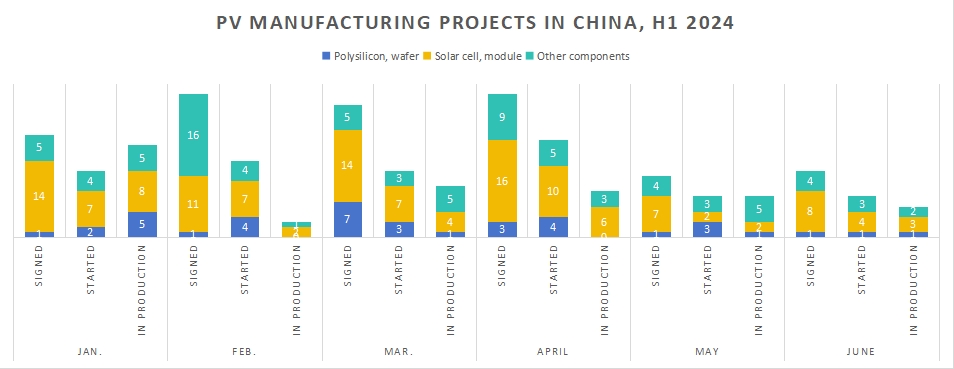

Solarbe’s latest data reveals a robust performance across the photovoltaic supply chain, encompassing 259 manufacturing initiatives. These include 127 newly signed projects, 77 projects breaking ground, and 55 projects commencing production, collectively representing an investment exceeding 790 billion RMB.

127 Signed Projects

During this period, 127 manufacturing agreements were inked, many surpassing 10 GW in scale and involving significant investments from industry leaders like Shijing Technology, Canadian Solar, Sunrev, and others.

Highlights include Yingfa Holdings‘ mammoth 320 billion RMB investment in a polysilicon, wafer, and solar cell facility. Qinghai Lihao also plans a substantial 250 billion RMB investment in high-purity silicon and industrial silicon production in Baotou.

Aiko announced a 100 billion RMB investment for a 25 GW high-efficiency solar cell facility in Anhui. Meanwhile, in Jiangxi, JTPV is investing 10.8 billion RMB in a 24 GW solar cell facility, and Linton NC is committing 10 billion RMB to a 200,000-ton ribbon production project.

The trend of collaboration between PV giants and diverse industries is noteworthy.

For instance, cable manufacturer Guizhou Changtong‘s 11.51 billion RMB initiative includes a 1.2 GW solar module production base and significant utility-scale solar projects in Guizhou.

Environment management service provider Shijing Technology and JinkoSolar jointly invested 10 billion RMB in a 20 GW solar wafer and cell project, while electrolytic aluminum producer Qiya Group plans a 10 billion RMB investment for a 20 GW wafer and assembly line in Sichuan.

Almost all of the 70 solar cell and module production projects focus on n-type technologies like TOPCon and HJT, underscoring a strategic industry shift.

Under the banner of vertical integration, JinkoSolar has scaled its n-type capacity to over 100 GW. Trina Solar aims to achieve over 80% sales from TOPCon products by 2024, with Canadian Solar and Aiko also expanding their TOPCon capabilities.

76 Facilities Broke Ground

In the first half of 2024, 76 new projects broke ground, with 28 undergoing environmental assessments and registrations. These encompass various stages from silicon wafers to modules, as well as ancillary materials like quartz sand, encapsulants, and frames.

Despite concerns about market saturation and price declines, investor confidence remains steadfast, fueling steady progress across multiple projects. The trend towards deeper integration within the solar sector continues unabated.

Trina Solar initiated construction on a 10 billion RMB vertically integrated facility in Yangzhou, set to produce 10 GW annually of large-format wafers, TOPCon solar cells, and high-efficiency modules upon completion.

Canadian Solar commenced an 8 GW wafer and cell project in February, slated for completion by October this year.

Risun launched a 25.4 billion RMB integrated PV manufacturing project in Baotou in March, covering extensive capacities across various segments.

Projects are also underway for critical components like backsheets, encapsulants, frames, quartz sand, and inverters.

54 Projects Started Production

In the first half of 2024, 54 projects commenced production, with investments exceeding 120 billion RMB. Capacity for solar wafers, cells, and modules surged to 150 GW.

Specifically, Tongwei and Hoshine made significant strides in polysilicon production, achieving capacities of 100,000 tons and 200,000 tons, respectively.

In the wafer segment, companies like Shuangliang, Honsun, Gaoce, and Unigrace New Energy launched operations, totaling 84 GW. Astronergy marked a milestone with its first solar wafer production at a 5 GW facility in Thailand.

In cells and modules, 25 companies initiated production, reaching a combined scale of 71 GW.

Heterojunction (HJT) technology emerged as a preferred choice due to its superior efficiency and cost-effectiveness. Companies such as Huasun, Soltrend, State Grid Energy Research Institute, and Akcome ventured into HJT cell production. State Grid New Energy’s 5 GW HJT project in Wenzhou and Akcome’s 4.6 GW HJT project in Ganzhou highlight this trend.

TOPCon modules accounted for approximately 41% of total production capacity, underscoring their growing significance in the market.

This surge in activity reflects China’s steadfast commitment to expanding its solar footprint amidst evolving global dynamics.

{kind=link}