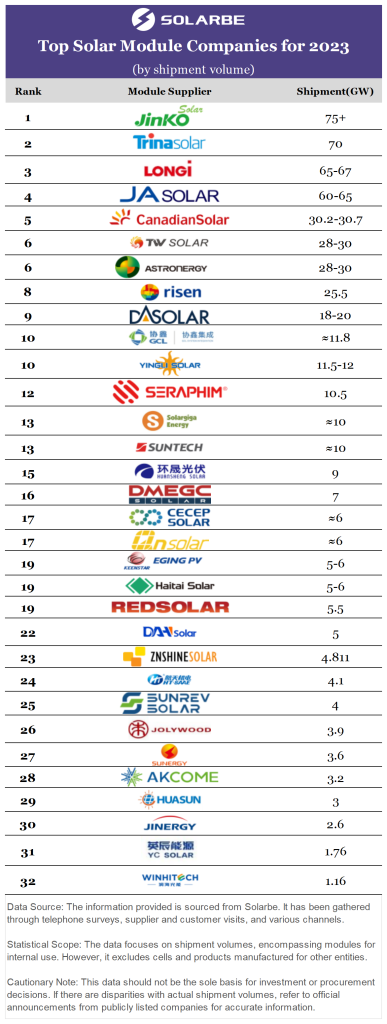

In the dynamic world of solar energy, 2023 proved to be a noteworthy year for the top solar module manufacturers. The recently unveiled shipment rankings shed light on the achievements of 32 companies, showcasing their strengths and strategies in the evolving solar industry.

Stability at the Top

The Top 4 and Top 5-9 lists remained relatively stable in 2023, with established and emerging brands holding their ground. JinkoSolar, Trina Solar, LONGi, and JA Solar collectively shipped over 270 GW, claiming a 52% market share.

The Top 9 brands, in total, surpassed 400 GW in shipments, securing a robust market share exceeding 75%.

JinkoSolar’s N-Type Focus Pays Off

JinkoSolar emerged as the leader in 2023, shipping over 75 GW of solar modules, with more than 60% being n-type products. This strategic emphasis on n-type technology positioned JinkoSolar as the industry leader in this category.

Leadership Trio: Trina Solar, LONGi, and JA Solar

Trina Solar, LONGi, and JA Solar demonstrated distinct product features and strong brand reputations, achieving success in both domestic and overseas markets. Trina Solar and JA Solar have accelerated efforts to expand n-type cell production, while LONGi is exploring advancements with back-contact (BC) cell technology.

TW Solar and Astronergy’s Progress

Among emerging brands, TW Solar and Astronergy showed momentum, with increased bid sizes compared to 2023. Both companies have set ambitious goals, aiming to exceed 50 GW in module shipments in 2024, even surpassing Canadian Solar, which targets between 42 and 47 GW. The competition for positions 5 to 7 in 2024 promises to be competitive.

Mid-tier Competition: Strategies Unveiled

Companies ranked 10th to 15th and 17th to 23rd engaged in fierce competition, recognizing the significance of every order in shaping their market position for the coming year.

Several companies, including Seraphim, Suntech, and DAH Solar, expressed plans to explore overseas markets in 2024, leveraging their positive brand image.

In bidding scenarios in China, mid-tier companies often quoted the lowest prices, actively competing for orders. Some companies in this range, starting from the third quarter of 2023, proactively reduced production rates and shipment targets, focusing on profitable orders.

According to industry insiders, in a market characterized by declining prices, companies with a singular production focus risk increased losses with higher sales volumes. These companies strategically abandoned expansion plans, trimmed costs, and aimed for higher profitability.

N-Type Market Surge: Vision for 2024

The adoption of n-type modules saw remarkable growth in 2023, with at least 7 companies reporting that over 50% of their sales comprised n-type products.

Despite the clear downward pricing trend and potential oversupply risks in the supply chain, numerous companies are steadfast in expanding their n-type production capacities.

Reports suggest that over 15 companies have set explicit targets for 2024, with n-type module shipments constituting over 60% of their total.

Among them, five of the top nine module manufacturers aim for an n-type share exceeding 70%, with three companies targeting an ambitious 100% by 2024, reflecting confidence in the future technological trends in the solar industry.

Innovators in the N-Type Arena: A Closer Look

Apart from the industry leaders, several other companies are making significant strides in the n-type segment:

- Solargiga Energy: Plans a significant upgrade and retrofit of existing production lines in 2024 to meet market demands, targeting an n-type module share of 60%.

- Suntech: Aims for a 70% share of n-type module shipments in 2024, with 16.5 GW of cell production capacity, a significant increase.

- Qn-SOLAR: Positioned as a TOPCon technology pioneer, aims to add 36 GW of n-type cell capacity in 2024, with an 80% share of n-type module shipments.

- DAH Solar: Achieved an industry-leading average conversion efficiency of over 26.4% in TOPCon cells. Targets 100% n-type module sales share with a combined capacity of 22.5 GW in four major bases.

- ZNShine Solar: Plans to establish a new 10 GW n-type TOPCon cell production capacity in 2024, aiming for an 80-90% n-type share.

- Huasun Energy: The only company to achieve a 100% n-type module share in 2023, continues to lead in HJT technology, with an increased shipment target for 2024 and an unwavering commitment to a 100% n-type share.

- WINHITECH: Anticipates a gradual increase in demand for high-efficiency HJT modules in 2024. Plans to expand production, achieving an n-type module share of around two-thirds of total shipments.

As the solar industry continues to advance, 2023 sets the stage for a competitive 2024, where each company will strive for a pivotal role in the ever-expanding global solar market.

{kind=link}